“When I started early in 2008, project managers were one of the groups I had to battle with,” said Holly Knight, Head of Sustainability at the Olympic Delivery Authority (ODA), at an

“When I started early in 2008, project managers were one of the groups I had to battle with,” said Holly Knight, Head of Sustainability at the Olympic Delivery Authority (ODA), at an

Thanks, James, for getting in touch with your questions. My views on this are as follows.

Thanks, James, for getting in touch with your questions. My views on this are as follows. You’ve actually got a couple of options and Mike Clayton talks about them in his book, Risk Happens! I’ve got that here. There are two ways really that he talks about including contingency in a cost breakdown structure, either at the level of tasks so you could either add in contingency for every amount on every lower level task, or you can add it at the top level, or you could add it at a subsidiary, middle level on the structure as well. So that was one alternative.

You’ve actually got a couple of options and Mike Clayton talks about them in his book, Risk Happens! I’ve got that here. There are two ways really that he talks about including contingency in a cost breakdown structure, either at the level of tasks so you could either add in contingency for every amount on every lower level task, or you can add it at the top level, or you could add it at a subsidiary, middle level on the structure as well. So that was one alternative. Mike, what sort of budget-related risks might projects face?

Mike, what sort of budget-related risks might projects face?Guessing is not a strategy: How to build decision velocity with AI and real-time data

June 10, 2026 | Live Webinar

Who really owns the project budget? Clarifying financial accountability

How to learn AI the sensible way

Making sense of project cost reports

How real PM mentoring actually works

The Accidental Product Manager: What project managers need to know

accounting, agile, ai, appraisals, Artificial Intelligence, audit, Backlog, Benchmarking, benefits, Benefits Management, Benefits Realization, Bias, books, budget, Business Case, business case, business case, Career Development, Career Development, carnival, case study, Change Management, checklist, collaboration tools, communication, Communications Management, competition, complex projects, Conferences, config management, consultancy, contingency, contracts, corporate finance, corporate finance, cost, Cost Management, cost management, credit crunch, CRM, data, data security, debate, Decision Making, delegating, digite, earned value, Education, Energy and Utilities, Estimating, events, FAQ, financial management, financial management, forecasting, future, GDPR, general, Goals, Governance, green, Information Technology, Innovation, insurance, interviews, it, Knowledge Management, Leadership, Lessons Learned, measuring performance, Mentoring, merger, methods, metrics, multiple projects, negotiating, Networking, news, Olympics, organization, Organizational Culture, outsourcing, personal finance, Planning, pmi, PMO, PMO, Portfolio Management, portfolio management, presentations, privacy policy, process, procurement, product management, productivity, Program Management, project closure, project data, project delivery, Project Success, project testing, prototyping, qualifications, Quality, quality, Quarterly Review, records, recruitment, reports, requirements, research, resilience, Resource Management, resources, risk, Risk Management, ROI, salaries, Schedule Management, Scheduling, scope, Scope Management, security, small projects, Social Impact, social impact, social media, software, software, software, Stakeholder Management, stakeholders, Strategy, success factors, supplier management, team, Teams, testing, testing, timesheets, tips, training, transparency, trends, value management, vendors, video, virtual teams, workflow

|

The overarching principle of the London Olympics has been to design with legacy in mind, and the desire was that the legacy was sustainable. The ODA is the government body responsible for the work in East London, effectively building the stage for a handover to LOCOG, the organising committee for the games. Think of LOCOG as an events company, Holly said, that would in turn hand over the location to the London Legacy Development Corporation to run the Olympic Park in the long term. “It was really important that when we started we had some strong leadership,” Holly explained. The team set high level strategic commitments for the programme, including 6 priority themes:

Each team in charge of a priority theme produced their own practical programme strategy, “a set of targets about how we were going to achieve it,” Holly added. The sustainability team took principles like One Planet living and used those as a basis for their targets and to set clear guidelines for what they expected from contractors. These were then used in the contract negotiations. The team also carried out what we would consider traditional stakeholder mapping, but called the resulting links “strategic alliances” (which is a term I like far more). “It was important that we did have relationships with groups like Constructing Excellence and the Construction Products Association,” Holly said, explaining that their stakeholder map was wide ranging and inclusive of industry bodies as well as those contractor groups directly linked to the work on site. Contracting the green wayThe Olympic programme had around £70bn worth of contracts across 50,000 contractual agreements. That’s a lot of paperwork, and a lot of contractors to get around spreading the word about the sustainability targets. The team needed to work on and with the supply chain, so they wanted to get sustainability into these contracts. “Procurement became one of our best friends,” Holly said. “The value of getting the procurement right was massive.” As a result, the sustainability team was fully involved in the contract negotiations. The selection criteria during the tendering stage included about 70% of measures for ‘traditional’ contract criteria and 30% on the priority themes, including sustainability. This meant that the priority themes and sustainability targets could be discussed with contractors in the very early stages and written in to contracts as appropriate. “But quite often when people turned up on site and we showed them what they had signed up for they didn’t realise,” Holly said. This was an issue when the sales and contracting team were a different group to the workers who arrived at the Park. As a result, there was a skills and knowledge gap. Holly explained that the sustainability team carried out a fair amount of “hand holding”. They ran workshops and delivered training so that the principal contractors knew what was expected and could cascade this information to the sub-contractors. The resultsThe sustainability team had 20 targets and sub-targets, and hit them all except for the sub-target around renewable energy. They smashed some, including the target for materials delivered by rail and water. They came in almost 30% higher than planned on that one. The velodrome is considered the most sustainable building on the park. The original steel frame roof structure was replaced with a cable net roof, which would not have been possible without excellent collaboration on the project between contractor groups. There were huge cost and health and safety benefits to making the change as well, so sustainability really does pay. Building sustainable structures also has a lower maintenance and electricity cost: for example, the swimming pool has removable ‘wings’. The venue needs 17,500 seats for the Olympics but other events only need around 3,000 – even events like the World Championships. So to keep the maintenance, heating and electricity costs down, the temporary stands will be removed after the event and the venue goes back to being a smaller space. A biomass boiler on the site reduces the carbon footprint but 30%. Overall, the programme has included some great leaps in sustainable design, and by planning this from the design phase of the individual projects, the London Olympics really can claim to be the greenest games yet. Photo credit: APM on Flickr |

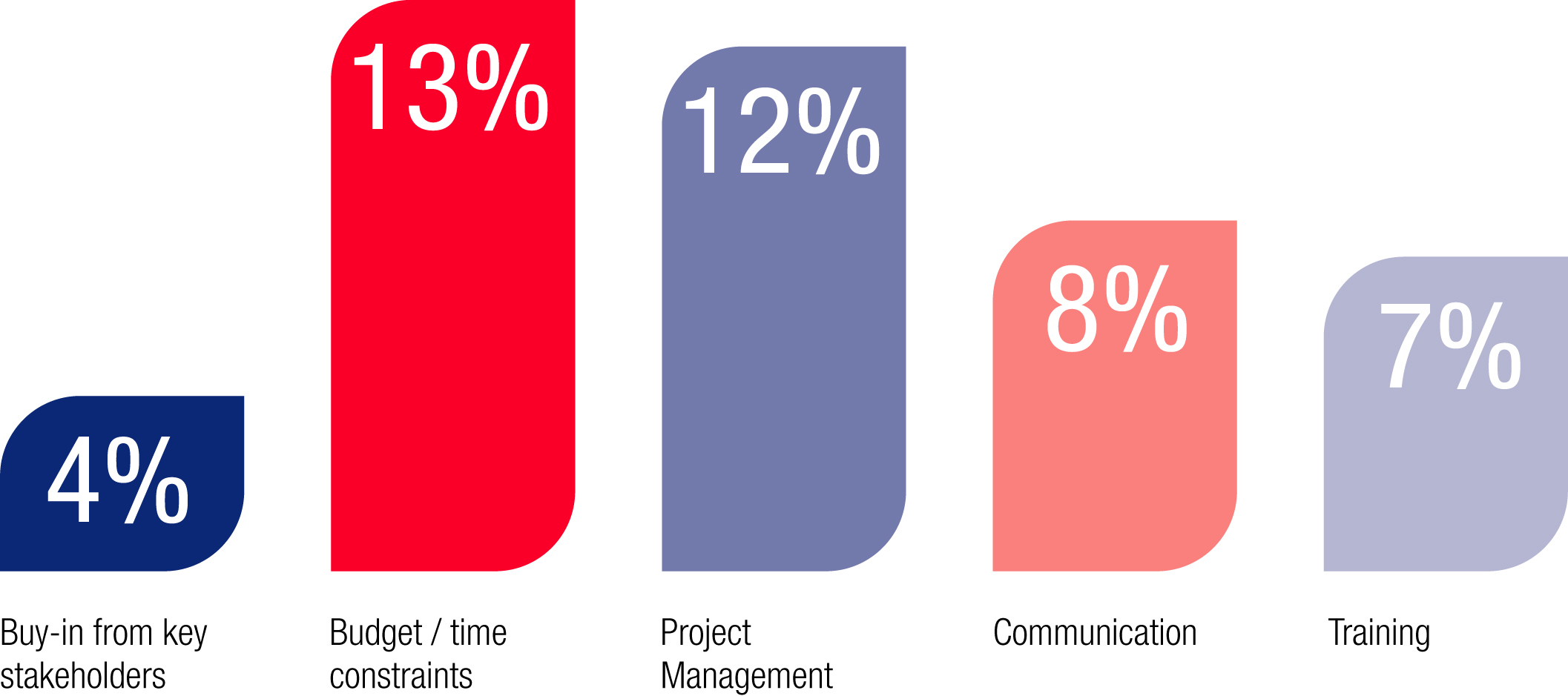

| ESI International, a large project management training company, released the findings of its latest annual benchmarking survey this month. “The State of the Project Management Office: On the Road to the Next Generation” survey investigates the current role of the Project/Programme Management Office (PMO), its development to full-blown maturity and value for the overall business. Based on responses from over 3,000 respondents in more than 17 industries on six continents, the research revealed that budgets have been the biggest challenge for PMOs over the last year. The survey respondents also said that in order to measure success, they relied on the standard definitions of the triple constraint: namely on time, to-budget project delivery. This is one way of defining success, and perhaps one of the easiest to measure but not the most effective (or modern) way of thinking about project success results. Maybe that’s why around 55% of respondents said that the value of their PMO was questioned by key stakeholders. Why might budget constraints be a top problem? Here are some reasons why budgets make the top of the list for PMO challenges:

Like all departments, PMOs are having to come up with new ways to do more with less. Maybe this is just a symptom that all departments are suffering from and is not a specific research finding related to PMOs. Is budget the top challenge for your PMO in 2012? If not, what is? |

| Every so often I’m asked questions about handling project finances. Here are a couple of questions from reader James about contingency budgets:

“In our construction project I put certain percentage of contingency into the budget for each individual job. This varies from one job to another in the budget, say 10% for job A, 8% for job B, 5 % for job C and etc. By adding each percentage, we can get to an overall figure, let's say $2 million. My questions are:

If job A completed and did not use the contingency budget, you should release it. If the contingency was set aside for a specific task and that task is now completed, you no longer need it. That is the 'proper' way to do it, because contingency is linked to risk. I assume that other project tasks are no more risky now, so you don’t need to keep that contingency to offset increased risk on the project.

However, in real life if your project sponsor will allow you to keep the money and you think it will come in handy then hang on to it! You never know what is coming up later, but don’t assume that you can spend it just because you have it. Hope that helps! If you have a question, drop me a line and I’ll try to include it next time. Or check out the previous episodes of the FAQ (links below) or the webinar on managing project budgets (which is free to watch). |

|

Video transcript, for those of you who prefer reading: Hello. My name is Elizabeth Harrin from the Gantthead blog, The Money Files and today I want to talk about cost breakdown structure. You have probably heard about work breakdown structure and product breakdown structure before but I wonder if you have heard of cost breakdown structure. Effectively it looks very similar to a work breakdown structure and you need a work breakdown structure to start with. Take your WBS, your work breakdown structure and add to each task your estimate of how much you think that task will cost to complete. Effectively, if you add on the values for each of those project tasks you’ll be able to work out at any level exactly how much the project will cost overall. The great thing about this is that you can add up the costs in chunks so you could create an overall cost for a work package or for a particular level of task. The good thing about that is that you can then use that to help influence your scope. For example, if your scope needs to be cut because you don’t have enough money to complete everything in time you could look at your overall work breakdown structure with the costs, your cost breakdown structure, and look at what you could potentially lose. Equally if you are including a change to the scope of your project you can look at what elements of costs would need to be changed as a result of adding something new on to the cost breakdown structure. You might be thinking that all sounds great but how do you add contingency to a breakdown structure that is constructed in that way?

But the option I like the best is this and his recommendation is this, to “add contingency at the level at which the budget will be managed. In this case” – in the example he gives in his book – “In this case the budget is managed at workstream leader level.” So what he has done in the example he has given here is to add contingency in the cost breakdown structure at the level at which somebody has responsibility for a chunk of work. So he has added contingency effectively to the task that is going to be managed by the workstream leader. And that has given him the opportunity to be able to give someone responsibility for managing the budget and be able to track that and use the contingency as they see fit within the remit of what’s on their element of the work breakdown structure. So I think cost breakdown structures could be a really good way to calculate your budget. |

| In this instalment of Ask the Experts I talk to Mike Clayton, author of Risk Happens!

“Cost over-runs” will be one of the first risks identified as soon as a project team starts brainstorming risks. Of course, it is not a risk at all, it is and outcome. Your question is critical – and to frame it in a more helpful way, “what are the uncertainties that can affect the financial outcome of a project?” Of course, the answer will be highly situational and depend on the nature and detail of your project, but here are a few of my favourites:

OK, that’s sensible. How can we better identify risk then, so that project managers don’t just stick with the force majeure items on their risk logs? There are lots of great techniques for identifying risks and it seems a shame to me how few are deployed on the vast majority of projects. We all know that brainstorming is a good – but not great – technique, yet it is still everyone’s favourite, in my experience. But, as you are asking about financial risks in particular, I want to advocate for a very powerful, yet easy to deploy, approach. Easy to deploy, that is, if you are planning your project well in the first place. Any substantial project must have a robust plan and at the heart of your planning process is a work breakdown structure (WBS). And it is only one more step to create a cost breakdown structure (CBS) that builds your project budget up, step by step from the components of your work packages. This works whether you are based in the US, where WBS tends to be built from a product based analysis or in the UK, where we would call that a product breakdown structure and build our WBS from a task orientation. Now simply review every item of cost on your CBS critically and ask:

Do you think Earned Value Analysis is a big help to project managers looking to manage financial risks on their projects? I look on Earned Value Analysis as the gold standard of the intersection between project delivery management and project financial management. It won’t so much reduce your financial risk as give you a powerful tool to spot trends that will allow the wary PM to act early to address time and schedule over-runs. Early action is at the heart of maintaining control and good information is essential for triggering the analysis that informed action needs. Where the overhead of implementing EVA is merited and the project team is fully trained, EVA is a tool for financial risk management throughout the delivery stages of your project. The delivery stage is a critical time, and that’s the point that conflicts arise between risk and return, when things are changing and stakeholders are keen to see progress. How can project managers handle that conflict? Firstly, by not thinking of it as a conflict! There is a rational judgement about a trade-off to be made, which must be informed by sound estimating based on the best available data and robust methods. That judgement must weigh risk and return and will often be a debate to be had within organisations. Your role as a project manager is to:

The “conflict” is a matter for good project governance. It sounds as if project managers need to spend more time thinking about project risk, to head off some of these problems and be better prepared to make these judgements. Yes. I think it interesting that the PMI’s Pulse of the Profession report for 2012 states that “change management and project risk management will become even more important core competencies” in 2012. That can only be a good thing. Whilst they remain the domains of Special Interest Groups within PMI and APM, too many project managers will see them as at best a specialist component to be delegated to a colleague and forgotten or, at worst, as an optional extra to project management. I would like to see more projects and programmes putting risk management front and centre of the processes, routines and behaviours. Thanks, Mike! Risk Happens! is published by Marshall Cavendish. Find out more at http://www.riskhappens.co.uk or check out Mike’s website at http://mikeclayton.co.uk/ |

|

"The higher up you go, the more mistakes you are allowed. Right at the top, if you make enough of them, it's considered to be your style." - Fred Astaire |