Guessing is not a strategy: How to build decision velocity with AI and real-time data

June 10, 2026 | Live Webinar

| last edited by: Peter Wootton on Mar 28, 2024 3:16 AM | login/register to edit this page | |||

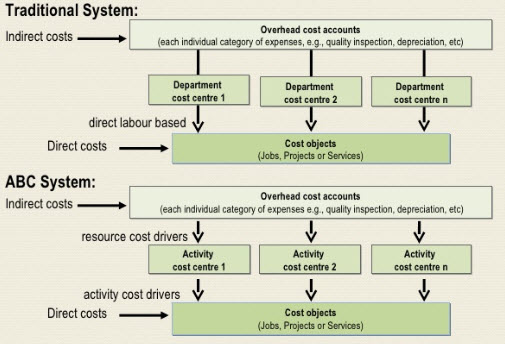

The accounting technique, which identifies all costs associated with individual activities comprising a project or process, irrespective of its place within an organizational structure. For example, ABC assigns product costs, based on the activities that are required to produce a product. By identifying the product’s cost drivers and its corresponding activities, this technique also allows for identification of non-value-adding activities and opportunities for cost reductions through reengineering or redesign. Activity Based Costing measures the cost and performance of activities, resources, and cost objects. Resources are assigned to activities, then activities are assigned to cost objects based on their use. Activity based costing recognizes the causal relationships of cost drivers to activities.

Procedures

InstructionsStart Activity Based Costing (ABC) by flowcharting the process, activity, or value stream. (See Work Flow Diagramming.) Information can be obtained from the financial reporting system or general ledger, as this keeps track of cost by cost element or expense category, (e.g., salaries, within large organizational unit structures). For every activity, identify the associated cost drivers. Costs that can be charged directly to activities include labor, capital, or other key resources. In addition, other costs include: depreciation, supervision, inspection, and maintenance, etc., to aid in the identification of costs for each activity.Sometimes it is necessary to define the resource drivers. A resource driver is used to assign costs from a general ledger orientation to an activity. A resource driver may include headcount, total number of desktop computers, and other sizing/value characteristics. For example, if headcount is a resource driver being mapped to an activity cost, it is necessary to determine a total number of people actually performing the activity. Dividing by the total headcount will give a resource costing rate. This figure can be mapped directly to the cost of performing the activity. Alternatively, costs or cost/resource drivers can be estimated during a work flow analysis session. This may be required when trying to determine the current status and a quick estimate of activity costs is required. Follow a similar procedure for each activity to identify fully-loaded costs. ABC assumes a causal relationship of cost drivers to activities. Management of these activities is the means to improving value received by the customer. During reengineering or redesign, ABC can be applied to identify the new costs (and, therefore, savings) for the proposed new environment. These new costs should be added to the new activity profiles to enable continuous improvement measurements. Non-value-added activities can lead to identifying possible areas of breakthrough for redesign.

Activity based costing often fails because project managers ignore the cardinal rule: It is better to be approximately correct than to be precisely inaccurate. When it comes to ABC, close enough is not only good enough; close enough is often the secret to success." Companies that implement activity-based costing run the risk of spending too much time, effort, and even money on gathering and going over the data that is collected. Too many details can prove frustrating for managers involved in ABC. Also to implement ABC, there needs to be specific systems in place, which could be costly when compared to the standard/ traditional. Another limiting factor is the 'time', where in usually projects are run at a fast pace that the PM does not have enough time to do a proper activity based costing

|

||||

| last edited by: Peter Wootton on Mar 28, 2024 3:16 AM | login/register to edit this page | |||

|

"No Sane man will dance." - Cicero |