Viewing Posts by Mario Trentim

The Differences Between Feasibility Studies and Business Cases

|

Before any organization undertakes a new project or initiative, it is essential to first assess the feasibility of that venture. This is done through feasibility studies and business cases:

Both are essential for any organization looking to undertake new projects or initiatives. Let’s look at these more in-depth: Technical Feasibility Studies Financial Feasibility Studies Operational Viability Studies Business Case In summary, here are the key differences:

Conclusion |

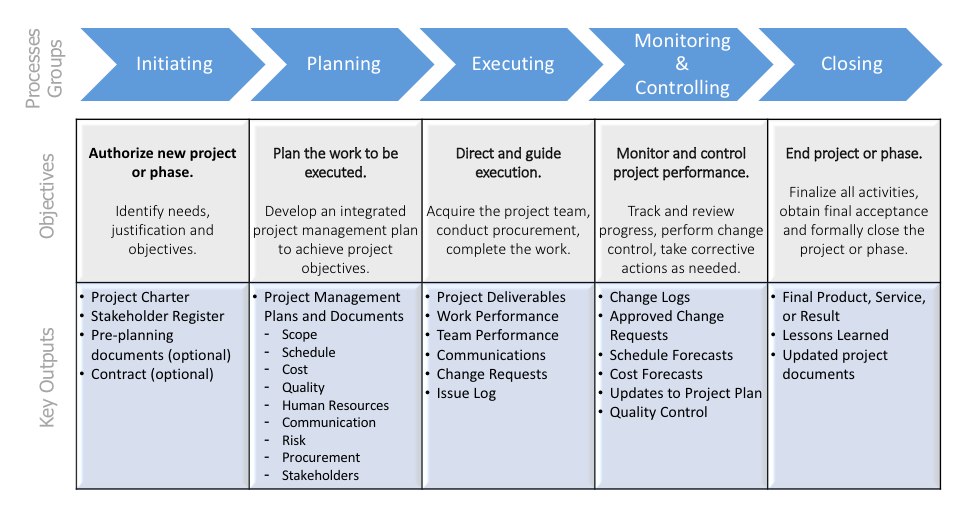

7 Steps to a Successful Project

|

In this post, I outline the key elements of any successful project. By taking the time to understand these steps and put them into action, you can increase the chances of your project being successful:

1. Define the goal of your project The goal of a project is to achieve a specific objective within a specified period of time. A project charter is a document that outlines the project's goals, objectives and timeline. It is an important tool for project management, as it provides a shared understanding of the project's goals and objectives. The project charter also helps to identify and track milestones, risks and costs. Without a clear goal, a project can quickly become derailed. Therefore, it is essential to define the goal of your project before beginning any work. 2. Gather information and research what has been done before Before embarking on any project, it is essential to gather information and research what has been done before. This will help you identify stakeholders, collect requirements and identify potential risks. It is also important to understand the current state of the project in order to develop an effective plan for execution. Without this information, it would be difficult to identify the problems that need to be addressed and the potential solutions that could be implemented. By taking the time to research and gather information, you can ensure that your project is well-informed and has a higher chance of success. 3. Develop a plan and timeline for your project A project plan is a critical component of any project. It sets forth the tasks that need to be completed, the order in which they should be done, the budget for the project, and the timeline for completion. Without a project plan, it is all too easy for a project to get off track and end up being delayed or over budget. Creating a project plan can seem like a daunting task, but there are a few key steps that can make the process much easier:

Once all of these pieces are in place, you will have a much clearer picture of what needs to be done—and when it needs to be done. With a well-developed project plan, you increase the chances of your project being successful. 4. Create a budget and find funding as necessary Any worthwhile project will require some level of funding, and it is important to estimate the cost of the project as accurately as possible before beginning to look for sponsors. In addition to the cost of materials, it is also important to estimate the duration of the project and schedule it accordingly. Once the cost and duration have been estimated, it is easier to create a budget and begin looking for funding. Although it can be difficult to find sponsors, there are a number of resources available to help with the search. Project management software can also be helpful in keeping track of expenses and ensuring that the project stays on schedule and within budget. By taking the time to estimate costs and create a budget, it is easier to find the funding necessary to complete a project successfully. 5. Assemble a team of experts to help Any successful project depends on assembling the right team of experts. But what makes a team effective? One key principle is understanding the stages of team development, first identified by psychologist Bruce Tuckman. Tuckman proposed that teams go through four distinct stages:

Effective team leaders recognize these stages and know how to manage them effectively. They also possess other key qualities, such as servant leadership and strong communication skills. By assembling a team of experts with these qualities, you can set your project up for success. 6. Implement the plan and monitor progress along the way A key part of successful project management is monitoring progress and making adjustments as necessary to ensure that the project stays on track. There are many different tools and techniques that can be used for this purpose, but earned value management is one of the most popular and effective methods. Earned value management is a technique that uses three measures—planned value, earned value and actual cost—to track progress and identify variances. By comparing the earned value to the planned value, project managers can track whether the project is ahead or behind schedule. Similarly, by comparing earned value to actual cost, they can identify any cost overruns. Thus, earned value management provides a clear picture of where the project stands at any given point in time and makes it easy to identify areas that need attention. As such, it is an essential tool for any project manager who wants to monitor and control the progress of their project. PRINCE2 and A Guide to the Project Management Body of Knowledge (PMBOK® Guide) are two other popular progress monitoring tools. 7. Get the final acceptance, then celebrate and close the project successfully These are the three keys to ending your project on a high note and setting yourself up for success the next time around. Of course, the best way to avoid having an underperforming project in the first place is to learn proper project management techniques and adopt best practices from the outset. But even if you find yourself in a difficult situation, all is not lost. By following these tips, you can ensure that your next project is a resounding success. Thanks for reading! Let me know if you have any questions about how to implement these processes or would like help assembling a team of experts for your next project…and share your own tips in the comments below! |

Virtual Teamwork Makes the Virtual Dream Work

|

My earliest experience with remote work came in around 2010. At the time, I believed it would enable me to connect with project teams from around the globe. What I considered a novelty has now become a new normal for myself and project professionals everywhere. With this shift comes the necessity to rethink leadership, collaboration and teams. A high-performing team can be defined as a group of people with clearly defined roles and complementary talents and skills, aligned with and committed to a common goal to innovate and deliver results. The importance of teams is not about to diminish as digital transformation reshapes the notion of the workplace and how work gets done. On the contrary, the (digital) leadership role becomes increasingly demanding as a diverse workforce, including freelancers and partners, works from home. It’s time that we adapt the essential characteristics of high-performing teams in the digital age:

Open and clear communication Maintaining an open-door policy can be a challenge in the modern workplace. Multiple notifications and meetings take a toll on productivity. High-performing virtual teams define ground rules for productive communication without abandoning social interactions. It’s possible to create water-cooler sessions, happy hours and the like to engage people on a personal level, while also keeping formal meetings focused on getting work done.

Solid team infrastructure Virtual spaces enable people to connect with other teams, yet it’s necessary to have clear roles and responsibilities just like those that existed in physical work spaces. Many-to-many interactions cause distraction and waste. Leaders must clearly define team topologies, boundaries and interfaces.

Positive atmosphere Working from home isn’t easy—and some people don’t get used to it. Trust, motivation and well-being are all deeply affected by remote work. So be sure to give those issues your attention by establishing the right incentives and offering feedback.

In a way, digital transformation empowers people to do more, extending and expanding capabilities. But it means nothing without strong leadership and clear communication.

How have you adapted your leadership style to best manage your virtual teams? Let me know your thoughts in the comments below. |

Building Effective Team Habits in the New Work Ecosystem

|

I’ve been familiar with remote work and virtual teams since 2010. I’ve also witnessed how digital transformation has enabled the adoption of new business models, flatter organizational structures and hybrid project management approaches since then. In the wake of the global pandemic, I’ve received many questions about building high-performing virtual teams, and how to improve collaboration and productivity as a whole in the workforce. Before I share some lessons learned with you, I’d like to remind you that we live in uncommon times. Predictions and models aren’t capable of guiding us as they were before the crisis. As quickly as teams have adapted to going virtual, there remains a great deal of uncertainty and a number of challenges that have yet to be overcome. Going back to January 2020, you and your team likely were used to working together in a particular context. Maybe you had flexible working hours, and some team members worked remotely. Perhaps you were all working 9 to 5 in the same physical office space. It doesn’t matter. What matters is that you had a routine. When the world came to a full lockdown, the concept of remote work and the modern workplace shifted dramatically. We also saw the shuttering of schools and places of business. I told my employees and team members in March: We don’t expect you to be as productive as you were in the office. Take your time, take care of your family and health. With time, people started adjusting and adapting to the so-called new normal—and forming new habits. There are many books and references about habit formation. I came across an insightful research article published by the European Journal of Social Psychology, which concludes that the repetition of behavior in a consistent context results in increasing automaticity and productivity. As we made our way in the new work ecosystem, we thought we needed some structured guidance. We addressed that with open discussions, one-on-one meetings, and a shared space for ideas, emotions and lessons learned about working from home.

New Habits for the New Normal Through a collaborative effort, my team built a work-from-home manual. It’s not mandatory, but it does provide some helpful advice:

Now I’d like to leave you some food for thought:

Let me know in the comments below. |

Defining a Standard Methodology and Project Management Metrics

|

Defining standards and metrics is a key function for the Project Management Office (PMO). In many ways, a PMO is uniquely positioned to provide guidance and orientation in order to build consistency in the application of project management best practices among the projects within an organization. As you can imagine, a standard methodology provides a basis for performance, and metrics provide a basis for the measurement of that performance against the standard. To that end, project management practices can benefit from metrics to establish the depth and extent of applying standards selected by the organization. Here, I will outline the steps in developing good PM methodology for your organization and how to define metrics and key performance indicators. Developing a Project Management Methodology The first step in introducing formal project management processes and practices is the awareness of the starting point (AS IS - current situation). The PMO should scrutinize the organization’s capabilities in the project management environment as a prerequisite for designing the type, depth and comprehensiveness of project management methodology processes and tools. The PMO’s examination of current project management practices involves the following activities:

Bear in mind that project management methodology development is not a simple task. This undertaking requires:

Below you can find a simple structure to guide you in developing a detailed methodology to suit your organization’s needs.

Defining Project Management Metrics The PMO will be involved in determining which metrics are used in the project management environment. Actually, most PMOs are responsible for metrics comprising the various sets of data that represent and quantify either its prescriptive practice guidance or results from its directed measurements. A good set of metrics can be used to:

Some metrics could be:

Defining a standard project management methodology is very important for consistency, helping to improve maturity and increase project success rates. This is a collaborative endeavor and should be led by the PMO, if there is one. What are some of your biggest lessons learned from developing standard methodology or defining project metrics? |